S&P500 LDN Open Trading Update 20/5/26

S&P500 LDN Open Trading Update 20/5/26

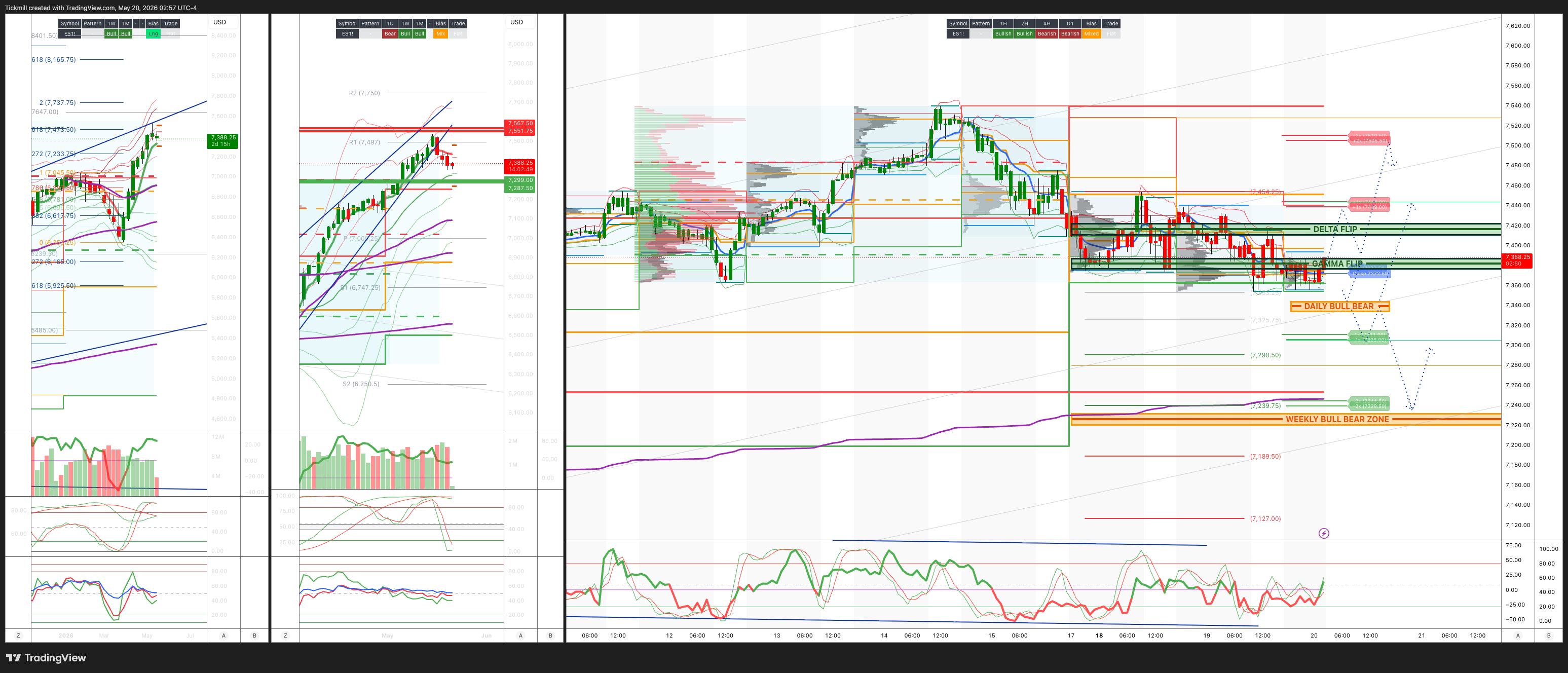

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7220/30

WEEKLY RANGE RES 7286 SUP 7550

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.23 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7434

WEEKLY VWAP BULLISH 7292

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFL - 7415

WEEKLY STRUCTURE – OTFH - 7363

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7350/60

GAMMA FLIP 7382

DELTA FLIP 7417

DAILY RANGE RES 7439 SUP 7306

2 SIGMA RES 7505 SUP 7239

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

LONG ON REJECT/RECLAIM WEEKLY BULL BEAR ZONE TARGET DAILY BULL BEAR ZONE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Mo’ Continued’

US equities closed weaker as the same two pressure points continued to dominate the tape: the momentum unwind and the rise in yields. The S&P 500 fell 67bps to 7,403 with a USD 1bn MOC imbalance to sell, the NDX lost 61bps to 28,819, the Russell 2000 dropped 101bps to 2,747, and the Dow declined 65bps to 49,364. Volumes were broadly in line with recent averages at 19.3bn shares versus a YTD daily average of 19bn. VIX rose 163bps to 18.11, WTI fell 82bps to USD 107.77, the US 10-year yield rose 7bps to 4.66%, gold dropped 184bps to USD 4,483, DXY gained 11bps to 99.30, and Bitcoin was nearly flat at USD 76,824.

The core issue is that the market is being hit by a factor correction at the same time as discount rates are moving higher. The US 10-year is now around 4.66%-4.67%, up roughly 45bps from the April lows. A two-standard-deviation rise in yields over a one-month period is historically difficult for equities, especially when leadership is narrow and concentrated in long-duration AI and semiconductor winners. The market is not yet in a disorderly selloff, but the rise in rates is clearly reducing tolerance for crowded growth exposure.

Under the surface, the momentum unwind remained the dominant feature. The buying frenzy into Semis and AI that characterized early April has faded materially. There is still a steady flow of capital into the AI complex, but the “manic” stopping-in behavior has tapered, leaving the trade more vulnerable to factor and quant-driven de-risking. Today’s TMT activity reflected that shift, with some buying in Software versus trimming in Semis. That looks less like a wholesale rejection of the AI thesis and more like a rotation within tech away from the most extended hardware/semiconductor exposure and toward areas where positioning is less extreme.

The levered semi ETF complex remains a source of volatility. Explosive volumes in products like SOXS stand out, and these vehicles can amplify intraday moves in the underlying semiconductor names. When flows into levered and inverse products increase during a momentum unwind, the feedback loop can become more mechanical: price weakness drives hedging and rebalancing, which can then create further underlying volatility. That argues for continued choppiness in Semis into NVDA earnings.

Consumer traded slightly better than the market, and today felt more constructive than yesterday. Initially, consumer strength looked like a simple byproduct of momentum unwinding, but the group now appears to be finding some independent footing. Flows were largely short covering and bottom fishing after better earnings from HD and AS. Home Depot was better than feared and offered positive commentary around May trends, while AS delivered solid results versus an elevated bar. The next tests are LOW, TGT, TJX, and VFC. Expectations appear highest for TGT, then TJX, then VFC, while LOW is expected to be closer to in-line. If these prints confirm that the consumer is bending but not breaking, the group can continue to catch a bid as investors look for alternatives to crowded AI leadership.

Flow activity was moderate. The floor was a 4 out of 10, finishing 120bps for sale versus a 30-day average of 143bps for sale. Asset managers were around USD 1bn net sellers, with broad supply across macro, tech, discretionary, and healthcare, and no major sector standing out on the buy side. Hedge funds were slight net buyers, driven by scattered short-cover demand in discretionary and software. This supports the idea that today’s market was not a capitulation event; it was more of a continued rebalancing away from crowded exposures, with some bottom-fishing in laggards.

After hours, CAVA traded up around 6%. The initial read is that results were good enough for now, though the call will matter. In a tape looking for consumer names that can still show demand resilience and unit economics discipline, CAVA’s reaction is relevant, but investors will likely need confirmation from management commentary before extrapolating.

In derivatives, the spot/vol relationship was less strongly positive than in recent sessions. Fixed-strike vols and spot both closed lower, though vols did catch a bid late in the afternoon as the selloff became more aggressive. SPX staged an impressive midday rally, led by momentum, which rebounded more than 7% from its intraday low. But the move in rates ultimately rattled the market, and equities closed in the red. SPX skew was bid across the curve, with flows tilted bearish through demand for both shorter-dated and longer-dated downside. At the same time, there were sellers of vol across the board, and activity was more concentrated in at-the-money buying versus wing selling. That combination suggests investors are still actively hedging but are trying to finance protection or avoid overpaying for far-tail convexity.

Thematic options activity remained focused on Semis, AI, and Energy, while demand for downside protection in Korea was also notable. Korea matters because of its memory and semiconductor supply-chain exposure; if the AI hardware unwind continues, Asian semiconductor markets can become a pressure point. Clients also used hybrid structures to express combined rates/equities views, which makes sense in a market where the equity drawdown is increasingly being driven by the level and speed of yield moves.

The main event is now NVDA after the close tomorrow. The implied move through Thursday is only 1.07%, which seems modest given the importance of the print and the recent volatility in the AI complex. The bar is high, but positioning has been partially cleaned up by the recent momentum drawdown. A strong print and guide could stabilize Semis quickly, particularly if NVDA confirms durable hyperscaler demand, supply visibility, networking strength, and margin resilience. But if the results merely meet elevated expectations, or if commentary raises concerns around memory shortages, gross margins, China, or capex digestion, the momentum unwind could extend.

The trading takeaway is that this is still not a broad “sell everything” market, but it is no longer a straightforward momentum chase. Rising yields are now a real constraint, and the speed of the rate move is especially problematic for long-duration growth. The AI theme remains structurally intact, but the near-term trade is crowded, volatile, and increasingly dependent on NVDA. Investors should avoid pressing oversized semiconductor exposure into the print, keep hedges in place, and use rallies to reduce factor concentration where positions are crowded.

At the same time, the rotation into Software and Consumer deserves attention. Software may offer a cleaner way to maintain AI exposure with less direct sensitivity to the levered semiconductor unwind, while consumer laggards with better-than-feared earnings can benefit from short covering and bottom fishing. Equal-weight and revision-supported laggards remain useful complements to AI exposure, especially if the momentum reversal persists. The market is digesting a simultaneous momentum correction and yield shock. Buybacks and earnings resilience are helping prevent a disorderly index decline, but the tape remains fragile. The next 24-48 hours matter: if NVDA validates the AI capex cycle and yields stabilize, the market can repair quickly. If rates continue higher or NVDA fails to clear the bar, the momentum unwind likely has further to run.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!