Dollar Down Sharply On Dovish Rates Repricing

US Inflation Plunges

The US Dollar is down sharply through the back of the week after suffering further heavy selling yesterday. The move lower comes amidst a wave of softer-than-forecast inflation data with both CPI and PPI undershooting forecasts this week. June annualised headline CPI fell to 3.5% from 4.2% prior, well below the 3.8% the market was looking for with core CPI also falling below forecasts. Yesterday, we then see monthly PPI data coming in below forecasts with the headline reading contracting 0.3%, a stark shift from the prior month’s 0.6% reading.

Fed Expectations & Repricing

The data has hit Fed tightening expectations hard with market pricing for a hike by year end dropping to around 75% from around 95% prior to Tuesday’s CPI release. This could mark an important turning point for the Dollar given the conversations we’ve heard recently questioning whether the build-up in hawkish expectations was too aggressive. The key driver behind the case for Fed tightening this year had been the run up in inflation as a result of soaring oil prices. However, on the back of the roughly 30% plunge in oil from YTD highs and the subsequent drop in inflation we’re seeing a dovish repricing in the outlook.

Oil Rising Again

If this dynamic continues to develop, USD could start to correct meaningfully lower. The caveat here is that we’re seeing oil prices rise once again as a result of renewed hostilities between the US and Iran. If this continues, this could reverse the current dovish repricing and push USD higher once again.

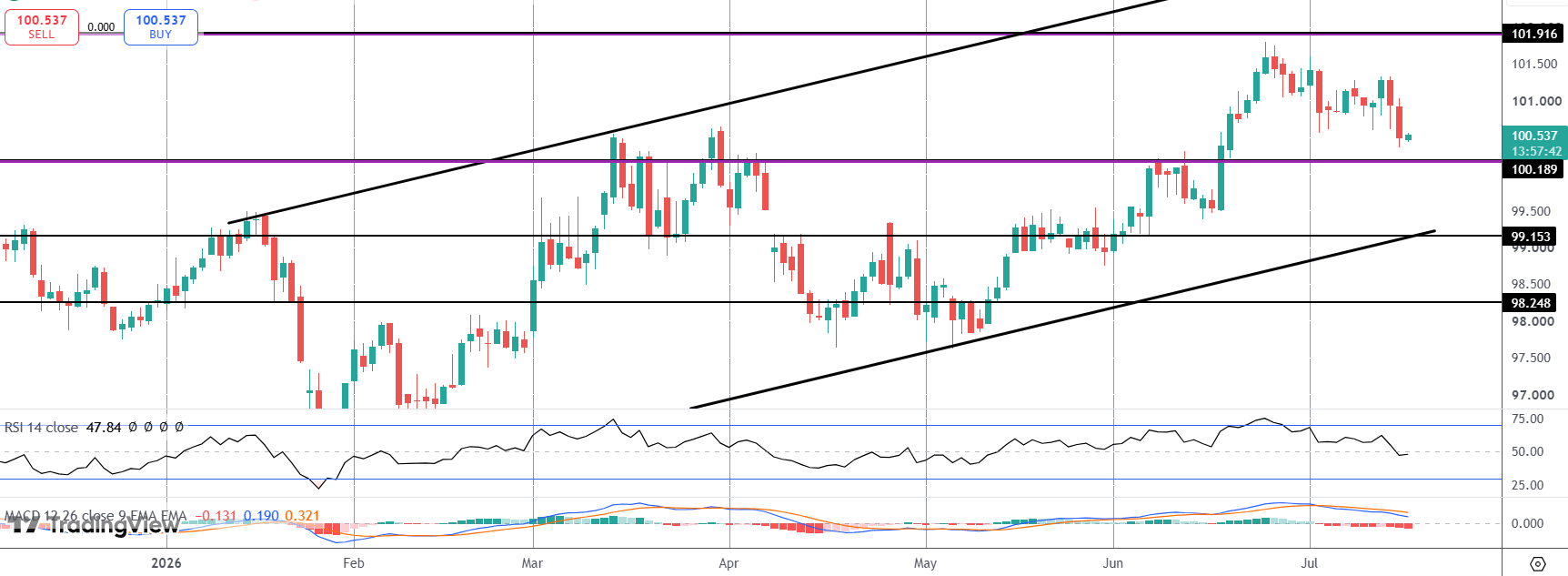

Technical Views

DXY

The index continues to reverse lower from the 101.91 level with price now fast approaching a test of the 100.18 level. This is key support for the Dollar and bulls need to defend this zone to maintain the broader bull outlook and prevent a deeper drop towards 99.15 and the bull channel lows.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.